Why America Needs Korea's Shipyards

The world's largest shipbuilder sits at the intersection of the LNG supercycle and a new era of naval rearmament. HD Hyundai Heavy Industries (329180 KR).

Disclaimer: Frontier Lane provides this content for informational and educational purposes only, not as investment advice. We hold no position in this security as of the publication date. Please read our full Disclaimer for more information.

The Shipyard at the Centre of Everything

On the southeastern coast of South Korea, in the industrial port city of Ulsan, sits a manufacturing operation of unprecedented scale. The Ulsan shipyard, operated by HD Hyundai Heavy Industries (HHI), spans 7.2 million square metres, or roughly 1,000 football pitches in size, along the coastline. It employs 15,000 people on site, building up to 20 mega-ships at any given time, each spanning 3 to 4x city blocks in length, delivering up to 50 vessels a year.

This is the largest shipbuilding complex in the world. Right now, it sits at the intersection of two of the most powerful structural forces in the global economy: first, the liquefied natural gas (LNG) supercycle; and second, the most significant Western naval rearmament push since the Cold War.

HHI was founded by Chung Ju-yung in 1972 at Ulsan, at a time when South Korea had virtually no shipbuilding industry to speak of. Within a decade, it was the largest shipbuilder in the world. Today, HHI is the flagship operating subsidiary of HD Korea Shipbuilding and Offshore Engineering (KSOE), which sits under the broader HD Hyundai group. (while sharing a founding lineage under Chung Ju-yung, HD Hyundai and Hyundai Motor Group are entirely separate entities with no cross-ownership or operational links). HHI specialises in the construction of large commercial vessels including LNG and LPG carriers, container ships, and crude tankers, alongside offshore production platforms, large marine engines, and naval ships ranging from patrol vessels to Aegis destroyers and submarines.

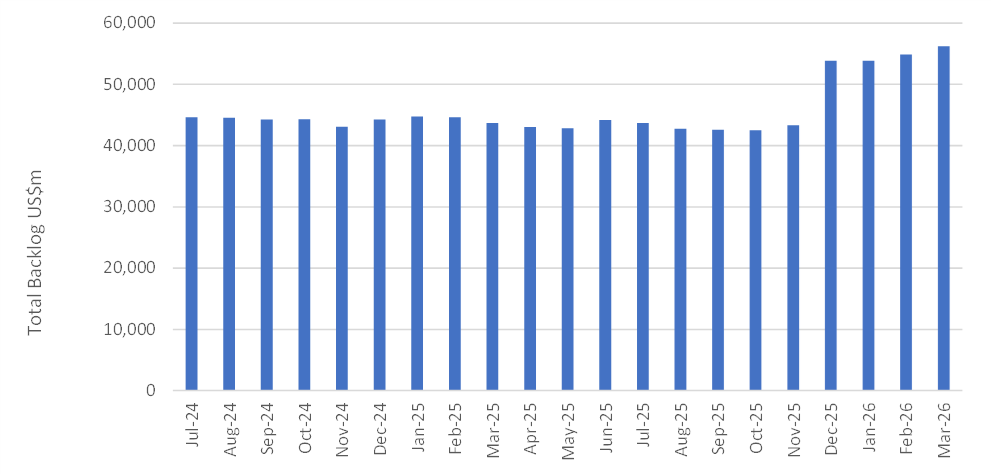

In FY 2025, HHI generated $11.9 billion in revenue, up 21% year on year, with an operating margin of 16% after years of near-zero returns. The backlog stood at $56.2 billion as of March 2026, with drydock slots booked through 2028 and into 2029. EPS grew 124% in 2025 alone. The share price has returned 445% over the past three years.

But the more interesting question is not where HHI has been. It is where it is going. Because the company is simultaneously navigating a renewed LNG carrier ordering cycle and an entirely new chapter in global naval rearmament, and the market, valuing HHI at roughly 21x forward P/E, appears to be pricing in neither with full conviction.

HHI is worth understanding for three reasons. First, it is deeply embedded in the plumbing of the global energy supply chain. The world has committed to moving enormous volumes of natural gas across oceans for decades to come, and only a handful of shipyards on earth can build the vessels that make this physically possible. HHI is the largest of them. Second, the company's defence pivot is happening at a moment when Western navies, particularly the US Navy, are running out of domestic capacity to build and maintain their own fleets. That is a strategic re-rating story, not a cyclical one. Third, the engine division is quietly finding early demand in land-based power generation for AI data centres, a vertical entirely uncorrelated to shipping cycles and one worth monitoring as it develops. Any one of these would be interesting on its own. The three together are what make HHI worth a deeper look.

HHI's shipbuilding capabilities

Source: Company filings.

Industry Dynamics: A Supercycle With New Rules

Shipbuilding is not like most industries. Ships take two to four years to build, revenue recognition is lumpy across that period, and quarterly earnings tell you almost nothing about the underlying business. The metric that matters is backlog, because backlog is the order book that has already been signed, and it determines what the income statement will look like for the next three years.

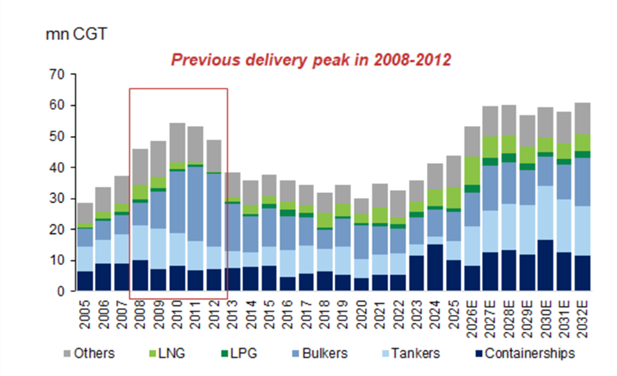

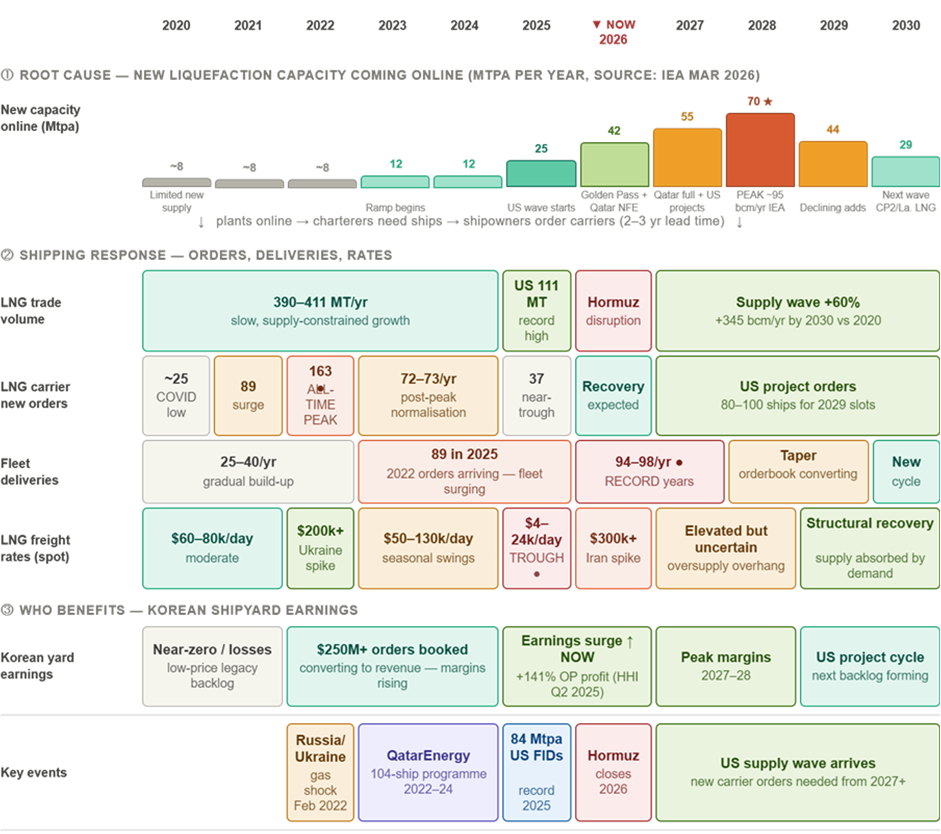

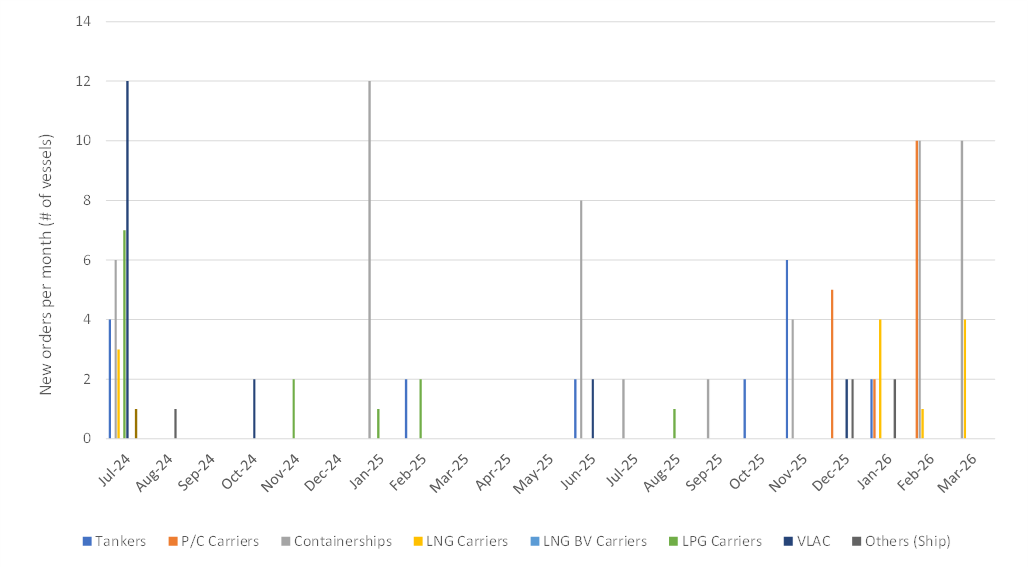

The current industry upcycle did not arrive in a clean upward line. The initial restocking wave began in 2021 and peaked in 2022, when a record 171 LNG carriers were ordered in a single year. 2023 and 2024 remained strong. But 2025 saw a sharp slowdown, with only 37 LNG carrier orders across the entire year, as shipowners absorbed earlier commitments and waited for newbuild prices to stabilise. The rebound is now underway: 35 LNG carrier orders were placed in Q1 2026 alone, nearly matching all of 2025. The takeaway is that the cycle is not a smooth arc. It is a structurally supported multi-year build-out punctuated by short pauses, and we are now exiting one of those pauses with momentum.

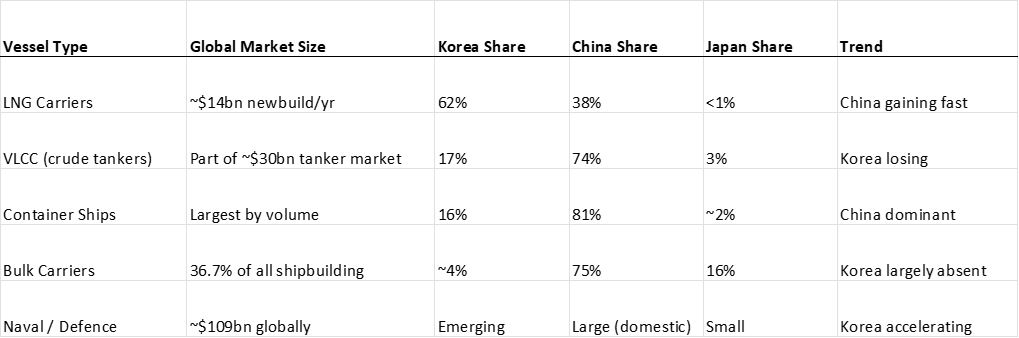

The global industry is dominated by three national clusters. Korea, China, and Japan together account for roughly 95% of all merchant tonnage produced worldwide. Europe retains a niche in cruise ships, with Fincantieri and Meyer Werft, while the United States is essentially a Jones Act-protected domestic market, structurally closed to foreign competition. Within Asia, the three clusters have diverged sharply over the past decade in ways that matter enormously to where the industry is headed.

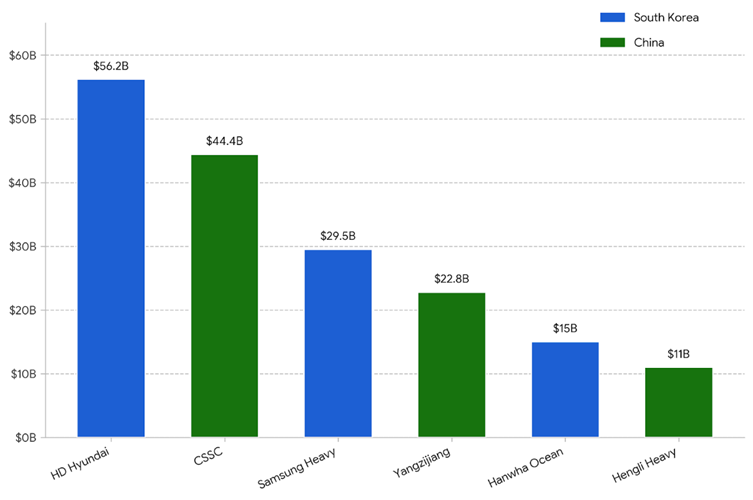

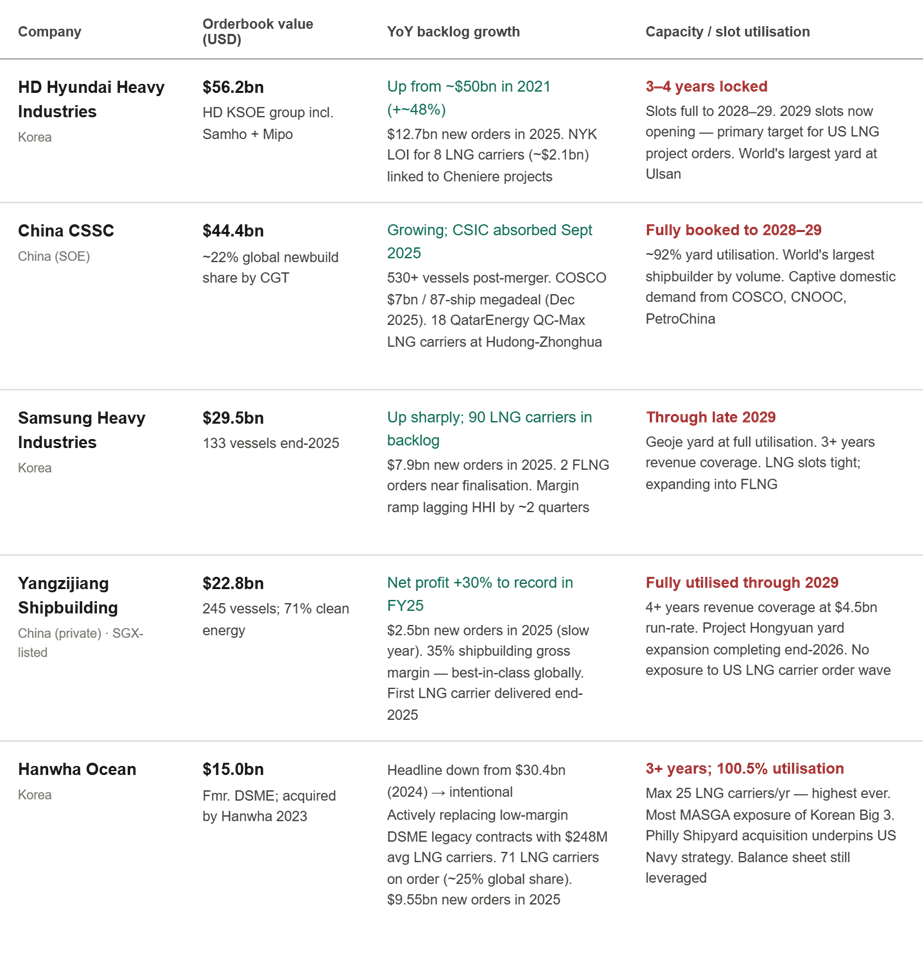

The world's largest shipbuilders, ranked by orderbook US$

China has built sheer volume. They now account for roughly 81% of global container ship construction and 74% of crude tanker production, driven by aggressive state-supported capacity expansion and competitive pricing on commoditised vessel types. Japan has faded, weighed down by an ageing workforce and limited capital investment. Korea has moved up the value chain. Korean yards have deliberately retreated from bulk carriers and standard tankers and concentrated instead on technically complex vessels where they hold deep accumulated expertise. The clearest expression of that strategy is LNG carriers, where Korea commands approximately 62% of global newbuild market share.

Global estimated shipbuilding market shares by vessel type

Global shipbuilding order backlog by type

Unlike the volume-driven commodity boom of 2008–2012, the current supercycle is propelled by a structural technology transition layered over a massive fleet replacement cycle. The International Maritime Organisation’s Net-Zero Framework mandates a 21% reduction in greenhouse gas fuel intensity by 2030, rising to 43% by 2035. This forces global shipowners to upgrade aging fleets to complex, alternative-fuel vessels capable of running on LNG, methanol, or ammonia. The LNG carrier segment highlights the extremity of this shift: with over 400 vessels currently on order, the backlog represents nearly 50% of the active global fleet, the largest in history. This shift plays directly into HHI’s hands; the required engineering depth, cryogenic containment expertise, and dual-fuel propulsion capabilities exist at only a handful of yards globally, with HHI leading the market.

Global shipbuilding annual deliveries by type

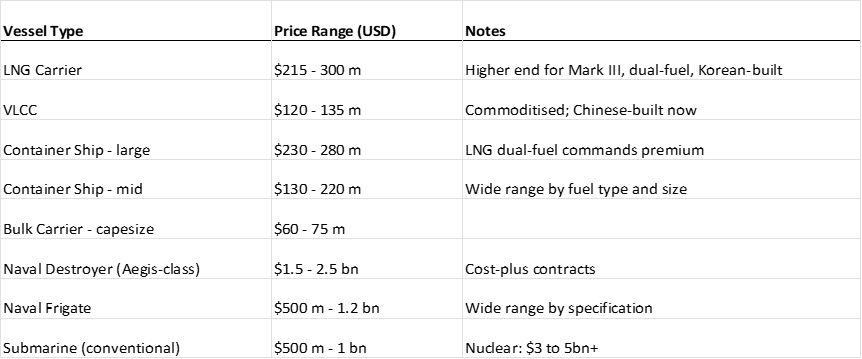

The numbers make this evident. A standard bulk carrier costs $60 to $75 million. A large LNG carrier costs $250 to $300 million, and the higher-specification Mark III dual-fuel variants built by Korean yards command closer to $300 million. That is 10x the price of a bulk carrier on a single vessel. Meanwhile, a naval destroyer runs to $1.5 to $2.5 billion. A frigate is $500 million to $1.2 billion. The entire economics of shipbuilding are being restructured around product mix rather than volume, and Korea, specifically HHI and its Korean peers, is best positioned to capture that shift.

Vessel price guide (US$ per ship)

Global shipbuilding orderbook breakdown

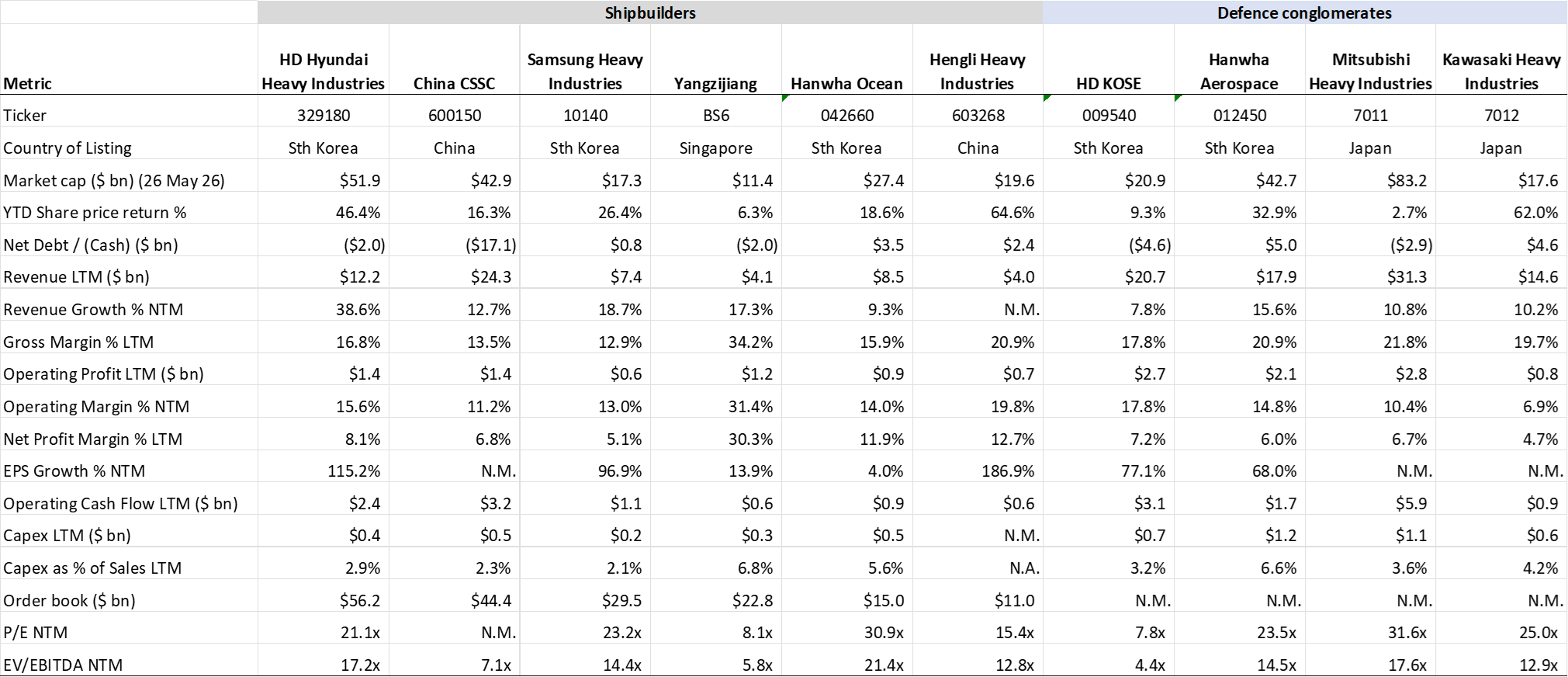

A look across the competitor landscape reveals a clear valuation disconnect. Despite leading the sector in scale and order book size, HHI lacks the defence premium assigned to its domestic rival, Hanwha Ocean. Because HHI's capacity is effectively sold out, management can selectively prioritise high-margin projects, giving operating margins a structural runway to expand. More broadly, Korean yards command a premium over Chinese peers due to their technical expertise in complex vessels, whereas Chinese builders face a persistent state-owned enterprise (SOE) discount and opaque disclosures regarding state defence projects. Given that pure-play defence contractors trade at significantly higher multiples than traditional shipbuilders, HHI's accelerating naval and MRO expansion presents a compelling case for a structural re-rating.

Peer benchmarking

HHI's Competitive Moat

Shipbuilding rarely captures the imagination of the generalist investor. It is easy to overlook the sector given its capital intensity, cyclicality, and sluggish pace, with assets that take years to construct and decades to depreciate. Yet, these exact frictions create formidable barriers to entry, effectively consolidating the global landscape into a tight oligopoly of just a handful of capable players. This concentration is precisely what makes the sector compelling to us right now. When a genuine supercycle intersects with a structural technology shift and a geopolitical rearmament wave simultaneously, the few yards possessing the scale to capture all three tend to generate returns that are anything but slow.

There is also a specific operating leverage dynamic worth understanding. Shipbuilding is a fixed-cost business. The drydocks, the cranes, the workforce, the engine plants are all paid for whether the yard is building bulk carriers at $70 million or LNG carriers at $300 million. When the mix shifts upward and pricing power returns, incremental revenue drops disproportionately to the bottom line. In the previous upcycle peak around 2010 and 2011, Korean shipbuilders generated operating margins above 10% before the volume-driven Chinese capacity expansion compressed pricing. The current cycle has the potential to exceed that, because the mix shift toward LNG, alternative-fuel vessels, and now naval work is more structural than the last commodity-led boom.

The question worth asking about any industrial business is not whether conditions are favourable. It is whether this particular company is the best-positioned to benefit from them. For HHI, the answer rests on four compounding advantages that are genuinely difficult to replicate.

Scale that cannot be bought overnight. Ulsan is not just the world's largest shipyard. It is a shipyard that has been continuously optimised for over fifty years. Building a comparable greenfield facility would cost $1 to $3 billion in drydock capital alone, and that figure does not include the decade or more required for classification society qualification of new vessel types, or the accumulated workforce expertise that only comes from building thousands of ships over generations. HHI's backlog of $56.2 billion, more than $10 billion ahead of China's CSSC and nearly double Samsung Heavy Industries, reflects the degree to which shipowners have already voted with their order books.

LNG cargo containment expertise. This is HHI's deepest technical moat, and the one most underappreciated by generalist investors. Building an LNG carrier is not like building a container ship at scale. Each vessel requires a precisely engineered membrane containment system capable of holding liquefied natural gas at minus 162 degrees Celsius. Constructing this system requires roughly 200 specialist workers executing precision welding and cryogenic insulation work over 18 months or more. Defects do not result in a recall. They result in boil-off rate penalties, owner claims, and reputational damage that can close a customer relationship permanently. HHI has been building LNG carriers for decades, holds approximately 35% to 40% of global LNG carrier newbuild order share, and has the track record that risk-averse energy majors require before committing a $270 million asset. This is not something a Chinese yard can replicate by hiring engineers and buying equipment. It takes time, and time is the one thing competitors cannot purchase.

Modular construction and the half-ship innovation. Rather than spending $1 to $3 billion on a new drydock to expand capacity, HHI has developed a modular construction approach where the stern of a vessel is fabricated at Ulsan and the bow at a separate fabrication facility, with the two halves married at a later stage. This effectively expands productive capacity without new drydock capital, and it is the kind of process innovation that requires deep manufacturing coordination capability to execute. Chinese yards, which have abundant drydocks, lack the modular sophistication. Japanese yards face workforce constraints that would limit execution.

Vertical integration through engines. HHI's Engine and Machinery division designs and manufactures large marine two-stroke engines, selling both into the captive shipbuilding business and externally to other yards. In 2025, this division expanded operating margins to 18.3%, well above the shipbuilding core. The integration provides a meaningful margin multiplier. When HHI builds an LNG carrier, they capture value on the hull, the containment system, and the engine. Competitors sourcing engines externally capture only the hull margin. Furthermore, in April 2026, HHI signed a $424 million contract with US firm Aperion Energy Group to supply 684 megawatts of HiMSEN engine capacity for data centre power infrastructure in Texas. This is the largest engine supply deal in the company's history and marks HHI's first entry into the US data centre power market. A follow-on MOU was signed in May 2026 between HD Hyundai Marine Solution and Aperion covering long-term maintenance for 33 power engines at the same Texas site. The deal is early and small in the context of group revenue, but it is the first concrete evidence that the engine business can find structural demand in land-based markets uncorrelated to shipping cycles. The market is not pricing this.

What the Market May Be Missing

The current HHI share price, at 21x forward P/E, reflects a well-run shipbuilder benefiting from a commercial cycle. What it does not appear to fully reflect is a structural re-rating driven by two forces converging simultaneously: the LNG ordering revival and the defence pivot.

The LNG upcycle is accelerating faster than expected. After a quiet 2025, when LNG carrier orders fell to 37 vessels for the full year, 2026 has reopened sharply. HHI's parent KSOE has already secured 16 LNG carrier orders year to date as of late May 2026, more than double its full-year 2025 volume of 7 vessels. Across the three major Korean yards, 35 LNG carriers were ordered in Q1 2026 alone, nearly matching all of 2025. The catalyst is straightforward. A massive wave of new global liquefaction capacity is coming online in 2027 and 2028, including the Golden Pass project in Texas, which began shipping LNG in April 2026, and major Qatari expansion projects. Shipowners are placing orders now to secure delivery slots for vessels needed to transport that supply. Furthermore, tightening environmental regulations are accelerating the obsolescence of older steam-turbine LNG carriers, compounding the replacement cycle. Crucially, Korean shipyards already have orderbooks extending through 2027 and 2028, meaning new orders placed in 2026 face delivery slots in late 2028 or 2029. HHI has effectively been at full capacity for over two years, which means management is now in the unusual position of picking and choosing the most profitable contracts to fill remaining slots rather than competing on price for marginal work. This is the structural backdrop behind the gross margin expansion described earlier.

Where we are at in the LNG cycle

The defence pivot is real, and the market has not priced it in relative to peers. This is the more consequential long-term story. HHI currently generates approximately $0.7 billion in defence revenue. The company is targeting KRW 7 trillion, or roughly $4.7 billion, by 2030. That is a 7x increase in defence revenue in five years, off a business that currently trades at 21x forward P/E, while defence focused peers including Mitsubishi Heavy Industries, Hanwha Aerospace and Kawasaki Heavy Industries trade at 25 to 32x forward P/E.

HHI targeting KRW 7 tn Defence revenues by 2030 ($4.7 bn), from currently $0.7 bn

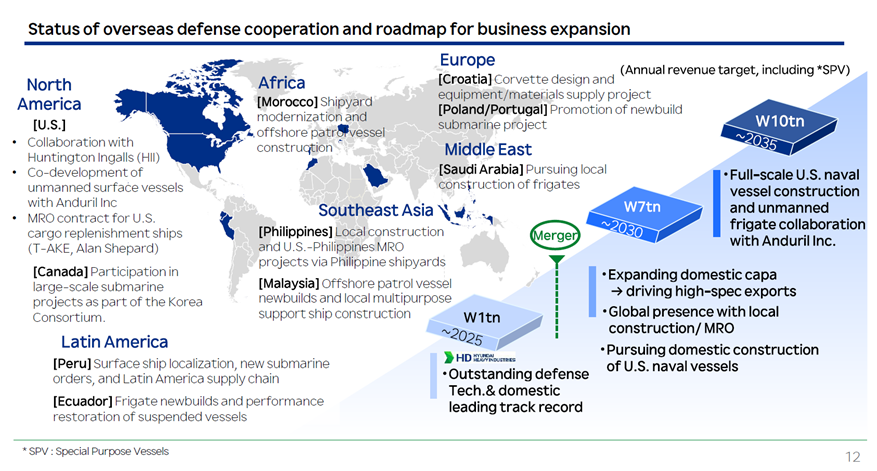

The foundations of this pivot are already concrete. In August 2025, HHI became the first Korean shipbuilder to sign a Master Ship Repair Agreement (MSRA) with the US Navy, securing an inaugural MRO contract for cargo replenishment ships. This entry point targets a severe US naval capacity crisis: decades of underinvestment have left American shipyards over-stretched and under-staffed, producing fewer than five oceangoing commercial vessels a year compared to China's hundreds. The US administration's Make American Shipbuilding Great Again (MASGA) initiative, a $150 billion cooperation framework between Washington and Seoul, is a direct response to this bottleneck. Crucially, while the Jones Act strictly prohibits foreign yards from building new vessels for US domestic use, the naval MRO market remains entirely accessible. By establishing a dedicated US subsidiary and partnering with Huntington Ingalls, HHI has smartly bypassed construction barriers to anchor itself in a global naval MRO sector projected to grow from $16.9 billion in 2026 to $24.8 billion by 2033.

Beyond the US, the government’s October 2025 "K-Defence" initiative aims to position South Korea as a top-four global arms exporter by 2027. HHI is already delivering tangible results, securing patrol vessel contracts for the Philippines, naval modernisation projects in Peru, and a spot on the South Korean consortium bidding for Canada’s $43.5 billion submarine program. The momentum is global: in Q1 2026, HHI broke into the historically Scandinavian-dominated icebreaker market with a $400 million Swedish contract. By April 2026, the company made its debut at Washington’s Sea Air Space exhibition, showcasing its Aegis destroyers and export submarines to 16,000 industry visitors and marking its arrival as a major sovereign defence player.

The December 2025 merger between HHI and sister entity HD Hyundai Mipo is the organisational step change that makes this credible at scale. Mipo's strength was mid-sized vessels, precisely the size profile relevant for naval MRO work. The merger doubled HHI's naval MRO dry dock capacity from 2 to 4. The Singapore hub formalised in August 2025 anchors the regional K-Defence expansion strategy across Southeast Asia, a market where HHI has now delivered 12 naval vessels to the Philippines alone since 2016. We track HHI's backlog, detailed below.

HHI Backlog US$

HHI New orders per month by type (# of vessels)

Hanwha Ocean remains HHI’s most direct defence competitor. Having aggressively pursued MASGA-related contracts and acquired Philly Shipyard as a US beachhead, Hanwha commands a premium 31x forward P/E, reflecting the market's enthusiasm for a naval re-rating. While HHI’s defence revenue is currently smaller and its multiple lower, this valuation gap represents a clear opportunity. Over the medium term, HHI’s combination of the world’s largest shipyard, deepest LNG expertise, and an accelerating defence portfolio should drive its multiple toward the 25x to 28x range of defence-adjacent industrials. While the commercial shipbuilding core anchors the valuation floor, the LNG franchise, engine optionality, and naval expansion are what will drive the multiple higher.

Key Risks

While HHI’s competitive positioning is strong, the thesis carries several structural and cyclical risks that warrant close observation.

China's Improving LNG Capability & Oversupply: The narrowing quality gap with Chinese yards (which captured 13 of the first 22 LNG orders in early 2026) poses a medium-term threat as they build a track record in membrane containment. Concurrently, the massive global LNG orderbook, representing nearly 50% of the active fleet, raises mid-term oversupply risks if demand slows. Key indicators to monitor include charter rates and US LNG project FIDs.

Chaebol Governance Discount: HHI is roughly 70% owned by KSOE within the Chung family-controlled HD Hyundai group. This structural complexity historically attracts a "Korea discount" due to minority shareholder exposure to group-level capital allocation. While the government's Value-Up initiative provides a tailwind, governance remains a friction on the multiple.

Foreign Exchange Fluctuations: While HHI enjoys a natural hedge by pricing products in USD, the 30% weakening of the Korean won over the past five years has been an artificial margin tailwind. A sharp appreciation of the KRW would rapidly compress operating margins.

Deep Industry Cyclicality: Despite structural drivers like environmental regulations and naval rearmament, shipbuilding remains highly cyclical. Any sharp slowdown in global trade or delayed energy infrastructure build-outs would quickly pressure the backlog trajectory.

Defence Execution Risk: Scaling defence revenue 7x to $4.7 billion by 2030 is an extraordinarily ambitious target. Early MRO contracts are small, the MASGA framework is non-binding, and rival Hanwha Ocean holds a structural edge via its domestic US shipyard acquisition.

Rather than a binary pass/fail, HHI's defence pivot should be viewed as a spectrum of valuation outcomes:

|

2030

Defence Revenue |

Investment

Profile |

Multiple

Justification |

|

~$1.5 billion |

Commercial

shipbuilder with a niche defence line. |

Fairly valued

at the current ~20x P/E. |

|

$2.5 to $3.0 billion |

Diversified

industrial platform with structural defence backing. |

Justifies a

partial re-rating to 25x – 27x. |

|

>$4.0 billion |

True

sovereign defence conglomerate. |

Full multiple

convergence with defence peers at 30x+.

|

The primary downside risk is not simply missing the absolute $4.7 billion target; it is a highly visible operational stumble, such as a lost MASGA contract or a delayed naval program, that prompts the market to strip away the defence premium entirely.

Valuation

Shipbuilders have historically been valued as cyclical industrials, with multiples that compress at the peak and expand at the trough. HHI followed this pattern precisely, trading above 35x forward P/E at the height of the 2021 enthusiasm before de-rating sharply through 2023 and recovering into the current cycle. At roughly 21x forward P/E and 17x EV/EBITDA, the market is pricing in continued operational improvement but not a structural re-rating.

The core thesis hinges on a single question: If HHI is evolving from a cyclical shipbuilder into a diversified industrial platform with a core defence anchor, what multiple does it truly deserve? While pure-play defence contractors routinely command multiples 30x and above, HHI is still being penalised by a traditional shipbuilder discount. A business generating billions in high-margin, double-digit defence revenue, layered over a dominant LNG franchise, presents a fundamentally different earnings profile.

Framing the upside against consensus forward EPS estimates of KRW 30,000 to 34,000 highlights a stark valuation gap:

|

Multiple

Scenario |

Justification |

Implied

Impact |

|

21x P/E

(Current) |

Market

continues to frame HHI strictly as a commercial shipbuilder. |

Broadly in

line with current price levels. |

|

25x P/E |

Modest

re-rating to the absolute floor of global defence peers. |

~20% upside

from current levels. |

|

28x P/E |

Partial

convergence toward domestic rival Hanwha Ocean's range. |

~35% upside

from current levels. |

Crucially, these targets do not require the 2030 defence pivot to be fully realised. They simply require the market to weight HHI’s changing product mix differently as defence revenue becomes a visible, recurring line item. A robust forward free cash flow yield, underpinned by drydock capacity booked through 2028, provides a firm valuation floor even if the re-rating takes time to unfold. Ultimately, realisation of this upside depends on three key catalysts: the pace of K-Defence and MASGA awards, the durability of the 2026 to 2027 LNG ordering momentum, and the market's willingness to abandon the legacy shipbuilder benchmark.

Conclusion

The setup for HHI is one of the more compelling industrial stories in Asia. While the broader industry spent the last decade contracting, HHI quietly reinforced its competitive moat. As low-cost competitors retreated to commoditised volume, HHI shifted its workforce and engineering capacity toward the exact high-value vessel types that are hardest to replicate.

Three tailwinds are now aligning simultaneously. The LNG franchise is exiting a short pause and accelerating into a multi-year ordering cycle backed by real liquefaction capacity coming online through 2028. The defence pivot from $0.7 billion to $4.7 billion is not a target on a slide; it is an actionable strategy backed by a merger, a US Navy MSRA agreement, and a dedicated Singapore hub. Furthermore, the engine division is running at 18% operating margins and opening its first land-based revenue streams in the US data centre power market.

The risks demand close monitoring. China's narrowing technical gap, chaebol governance frictions, and ambitious execution timelines are real. But HHI possesses the balance sheet strength, backlog visibility, and engineering depth to navigate each from a position of genuine industrial dominance.

Make no mistake. This is the world's largest shipbuilder sitting at the precise intersection of global energy infrastructure renewal and Western naval rearmament, and it still trades at a discount to both peer groups. The structural transition is already underway. The multiple gap between where HHI trades today and where it belongs is the opportunity.

Appendices

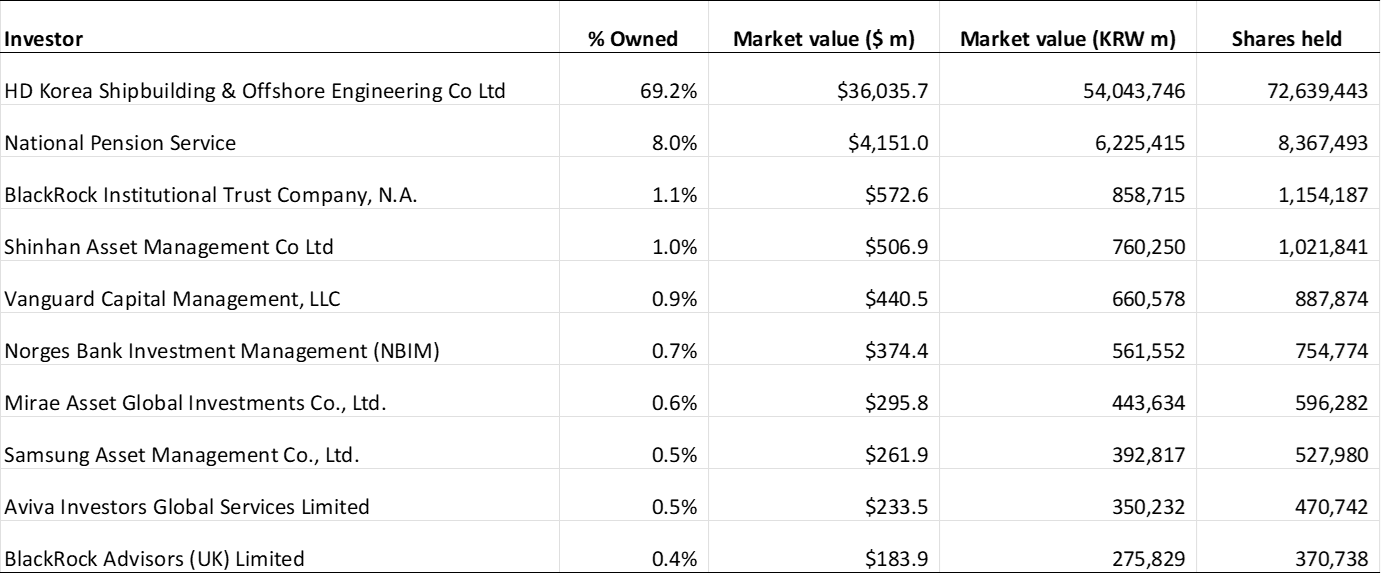

Top shareholders

Enjoyed this research?

Receive our future Research and Frontier Briefings.

Frontier Lane also works with a select group of long-term investors, founders and family offices on capital allocation and investment strategy.