Meta pivots into cloud infrastructure business; OpenAI considers US government a stake

We look at Meta's cloud ambitions, Washington's potential stake in OpenAI and how small engines are solving an energy bottleneck.

In this Frontier Briefing, we wrap our heads around the massive volume of capital pouring into AI infrastructure and the regulatory ripples changing the playing field. It is a noisy market right now, so we’ve distilled the developments actually worth your time below.

Meta plays a new hand in the cloud wars

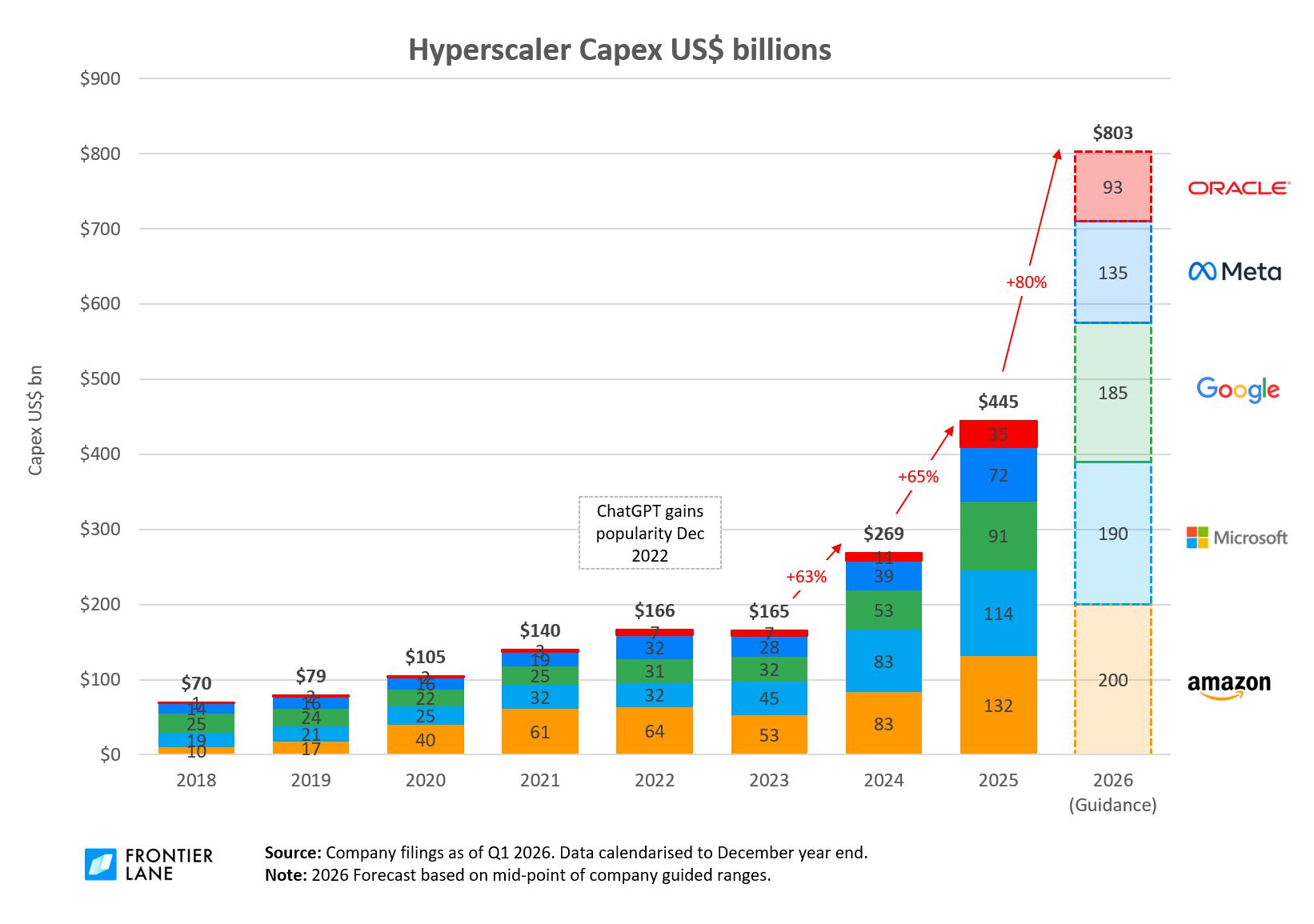

The market has spent the last years anxious about the sheer scale of capital expenditure that tech giants are pouring into artificial intelligence infrastructure. We track hyperscaler capex spend every quarter, and this year total capex spend across the hyperscalers will be over $800 billion, up 80% from last year. Capex has increased by almost 5x over the last 3 years.

Meta has been at the centre of this storm, spending heavily on GPUs with no immediate line of sight to direct infrastructure revenue. The report that Meta is developing a cloud business, Meta Compute, to sell access to its excess AI capacity completely changes this dynamic. Meta stock was up 9% following this news.

By offering third-party access to its massive reserves of compute, Meta is turning a cost centre into a potential profit engine. This move serves as a direct hedge against their own internal development cycles. If their own consumer-facing AI features do not monetise as quickly as expected, they can simply rent the underlying compute to enterprise customers. The inflection point to watch will be the initial pricing structure of Meta Compute. If they undercut the dominant public clouds, it will confirm a structural shift in how enterprise compute is priced.

For investors, this creates a distinct divide. While it is highly bullish for Meta's margins and capital efficiency, it presents a serious headwind for the venture-backed neoclouds that have popped up solely to rent out GPUs. When a giant with practically free cash flow decides to dump its excess capacity onto the open market, smaller players with high cost of capital get squeezed. We favour Meta on this development, whilst remaining highly cautious on pure-play GPU-rental platforms.

Washington’s potential 5% slice of OpenAI

In a move that sounds more like state-directed capitalism than Silicon Valley tradition, OpenAI has proposed giving a 5% equity stake to the US government. The idea is that sharing the wealth generated by AI with the public could help address some of the pushback against the technology, which threatens jobs in many industries and has potentially wide-ranging implications for national security.

The inflection point is whether Congress or the administration officially accepts this structure, and under what oversight terms. The 5% stake would be worth around $43 billion, based on the last funding round in March, which valued OpenAI at $852 billion. We think that these negotiations is also a contributing factor as to why OpenAI decided to pause it's IPO plans this year.

If approved, it sets a massive precedent. It could also mean other AI frontier labs following the same equity ownership model.

Small engines solve a massive grid lock

The physical constraint of the AI boom is not just silicon; it is power. As data centres face lengthy delays to connect to national electricity grids, operators are taking matters into their own hands. In a less-covered trend, small engine makers are gaining massive momentum as data centres look for cheap, readily available off-grid power solutions.

These modular, small-scale engines allow developers to build out capacity without waiting years for utility companies to upgrade substations. This is a classic second-order play. While the market focuses on green energy transitions and mega-nuclear projects, the immediate, pragmatic solution to keep servers spinning is highly distributed, localised power generation.

This dynamic creates a highly defensive investment thesis for industrial engine manufacturers like Caterpillar (CAT) and Cummins (CMI). These businesses have traditional cyclical profiles, but they are now receiving a structural demand boost from the tech sector that is completely disconnected from the broader macroeconomic cycle. We expect this tight supply of on-site power equipment to persist over the next year.

A new era of US trade protectionism arrives

The decision by Washington not to grant a long-term renewal to the North American trade deal (USMCA) marks a major shift in trade policy. By moving the agreement to annual rolling reviews, the administration has introduced a permanent state of negotiation and uncertainty for businesses operating across Canada, Mexico, and the United States.

This is a deliberate strategy to keep maximum pressure on America's trading partners, particularly regarding trade deficits and the rules of origin for automotive manufacturing. The inflection point will be the upcoming annual review cycles, where US negotiators are likely to demand significant concessions to protect domestic manufacturing jobs.

The immediate victim of this policy is Mexico's nearshoring thesis. The country had become the default destination for companies looking to bypass Chinese tariffs while maintaining easy access to the US consumer market. With the USMCA now under constant review, multinational corporations will have to price in a higher political risk premium for Mexican operations. We are focusing on highly automated, domestic US manufacturing plays.

Private credit faces a reckoning in the software roll-up space

The rapid rise of private equity-backed software roll-ups has been fuelled by cheap, abundant private credit. For years, this was a highly profitable ecosystem, but we are starting to see the first real cracks in the foundation. The recent financial distress at Medallia, a major enterprise software business, has sent a chill through the private debt markets, illustrating the risks of high leverage in a higher-for-longer interest rate environment.

The core issue is that many private-equity managers have been collecting lucrative fees on paper gains, valuation marks that they determine themselves, while the actual underlying businesses struggle to generate the cash flow required to service their debt. The inflection point will be when these semi-liquid funds face rising redemption requests, forcing them to either write down valuations or sell assets into a illiquid market.

This environment will distinguish the disciplined credit managers from the asset gatherers. We are avoiding highly leveraged software roll-ups and the private credit funds that backed them at aggressive multiples. Instead, we favour public asset managers with conservative balance sheets and liquid, transparent portfolios that can benefit from the eventual restructuring of these distressed private assets.

The rise of Bending Spoons and the public roll-up model

While traditional private equity faces headwinds, the public markets are showing a strong appetite for a different kind of tech consolidator. The successful Nasdaq debut of Bending Spoons, which saw its shares surge 40%, highlights a growing trend of public tech roll-up vehicles. The Italian group, known for acquiring legacy consumer software brands like Evernote and StreamYard, has proven that disciplined, programmatic software acquisition can thrive under public scrutiny.

Unlike private equity funds that rely on heavy leverage and long holding periods, public roll-up vehicles can use their own highly valued stock as currency for acquisitions. They focus on aggressive cost-cutting, product simplification, and pricing power. The inflection point to watch is whether they can successfully transition these acquired utility apps into long-term cash generators, or if the user bases eventually decay.

We see this as a highly scalable model in an environment where venture capital has dried up for mid-tier software companies. Founders looking for an exit have fewer options, allowing disciplined consolidators like Bending Spoons to buy cash-flowing assets at highly attractive valuations. We expect to see more of these public vehicles emerge, presenting a unique, liquid alternative to traditional private equity exposure.

Closing thoughts

As we move into the second half of the year, the easy consensus trades are beginning to fracture. The simple formula of buying raw AI capacity and hardware is giving way to a more disciplined focus on operational integration, energy logistics, and capital efficiency. Meanwhile, the changing political landscape in Washington is beginning to leave its mark on trade structures, national security spending, and the corporate governance of our most valuable technology firms. We continue to favour businesses with tangible infrastructure moats, proprietary data applications, and resilient, domestic supply chains. We will be monitoring the upcoming US employment data and the initial pricing announcements from the emerging cloud providers closely.

Enjoyed this research?

Receive our future Research and Frontier Briefings.

Frontier Lane also works with a select group of long-term investors, founders and family offices on capital allocation and investment strategy.